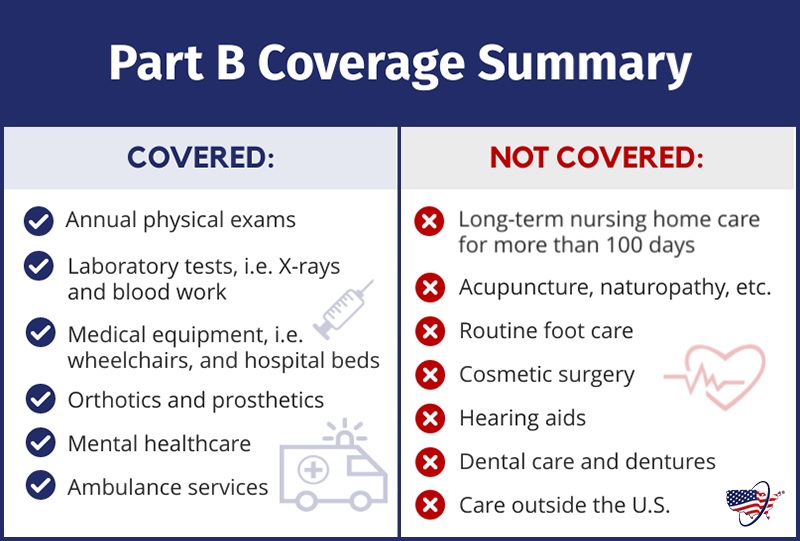

Enrolling in a medical insurance policy may not always cover all your Medicare costs. In fact, a minimum of 20 percent is not covered, along with the costs of the prescribed medications. The old healthcare policies did not place any limit on people’s out-of-pocket expenses. So, people began wondering what they needed to do to cover the medical costs that were not covered by their insurance policies. Here are a few methods to handle this situation:

Get a medical insurance supplement

For the beneficiaries of the federal insurance policy, there is no additional policy. Therefore, they have to subscribe to schemes with supplemental policies. In fact, this extra policy covers deductibles, copayments, and coinsurance. With such a scheme, there will not be any unpleasant surprises or additional costs for home visits or even follow-ups. Just because the supplemental policy does not cover medical treatments does not imply that it cannot extend the coverage of some extra time spent at the hospital or costs beyond the federal insurance policy limit. This is just one of the Medicare Advantage plans 2025.

Take advantage of the supplemental policy

Even though the premiums keep on increasing each and every year because of the increasing age of the subscribers, the premiums may differ depending on various factors such as gender, smoking status, age, and whether you reside in your house together with your spouse. However, you will have three primary rating options in front of you. One of them is called the “community rating,” wherein the premium paid by everyone will be the same as that of the others, irrespective of their ages. The second rating is called the “attained age,” wherein the costs of your insurance will increase as you age. The third kind of rating is called the “issue age rating,” wherein the age at which you took the premium is its basis. While purchasing policies, make sure that you consider the premiums over the lifetime of the policy.

Decide the best time to buy insurance

It would be best to purchase an insurance cover during the six-month Open Enrollment period so that you would not be denied coverage on the basis of any of your pre-existing health conditions. The insurer will cover all of your pre-existing health conditions if you buy an insurance policy during this period. Furthermore, subscribing to the supplemental policy will ensure that no questions are asked about your vital statistics, no matter what. Furthermore, you will not be charged a penny more, irrespective of all of your health problems.

However, if you are suffering from a disability, it would be best to speak to your insurance advisor since he can help you cover the 20 percent that your policy does not cover by comparing all the different policies. Each state in the United States of America has a different policy regarding premiums. While some states charge you more, others charge you less. Thus, you will be able to save money and also cover the costs that your primary federal health insurance policy does not cover.